$230 Trillion in Assets. Only 11% Eligible as Collateral. That Gap Won't Survive the Decade.

Published • 10 Apr 2026

6 mins

There are roughly $230 trillion in global marketable securities, but the collateral market is only about $25 trillion.

This isn’t about technology. It’s the infrastructure. And it represents a $205 trillion eligibility gap that is now attracting the attention of every major bank, asset manager, and regulator.

The World Economic Forum's 2025 report on asset tokenization outlined the scale: collateral markets exceed $25 trillion in value, with the repo market alone surpassing $15 trillion in outstanding value and $3 to $4 trillion in daily turnover. And yet, most of the world’s securities are still not efficiently used as collateral, not because they lack value, but because the infrastructure around them still doesn’t work smoothly. Settlement systems, custody layers, and jurisdictional fragmentation keep that capital from moving freely.

That infrastructure is changing. The institutions that move first will define the new standard. The rest will adapt to it.

The collateral tax nobody budgets for

Collateral management should be basic infrastructure. It isn’t meant to be a source of systemic risk. Yet three times in the past five years, collateral systems have amplified rather than absorbed market stress: the March 2020 “dash for cash,” the 2022 UK gilt crisis, and the energy margin shocks following Russia’s invasion of Ukraine.

The mechanism is always the same. Markets move fast. Margin calls spike. The collateral system, built on T+1 or T+2 settlement cycles, manual reconciliation, and fragmented custodial workflows cannot keep up.

ISDA's 2024 margin survey puts numbers behind the pressure: 32 leading derivatives firms collected $1.5 trillion in margin for non-cleared derivatives, up 6.4% year-over-year, with another $390 billion posted to central counterparties for cleared trades. At the same time, the composition of that collateral is shifting under stress. Cash’s share fell to 51.3%, its lowest level on record, while non-government securities rose to 13.8%, the highest in six years of ISDA tracking.

The market wants a broader collateral base. The plumbing cannot deliver one.

Money market funds worth trillions of dollars in stable, low-volatility assets cannot simply be posted as collateral between counterparties today. The adjusted value must first be converted to cash, then transformed by a custodian. ISDA describes this as a multi-step workflow that introduces liquidity and operational risk precisely when you need to eliminate it.

The WEF estimates that distributed ledger-based collateral management could free up more than $100 billion annually in trapped capital.

Proof of concept is over. Deployment is underway.

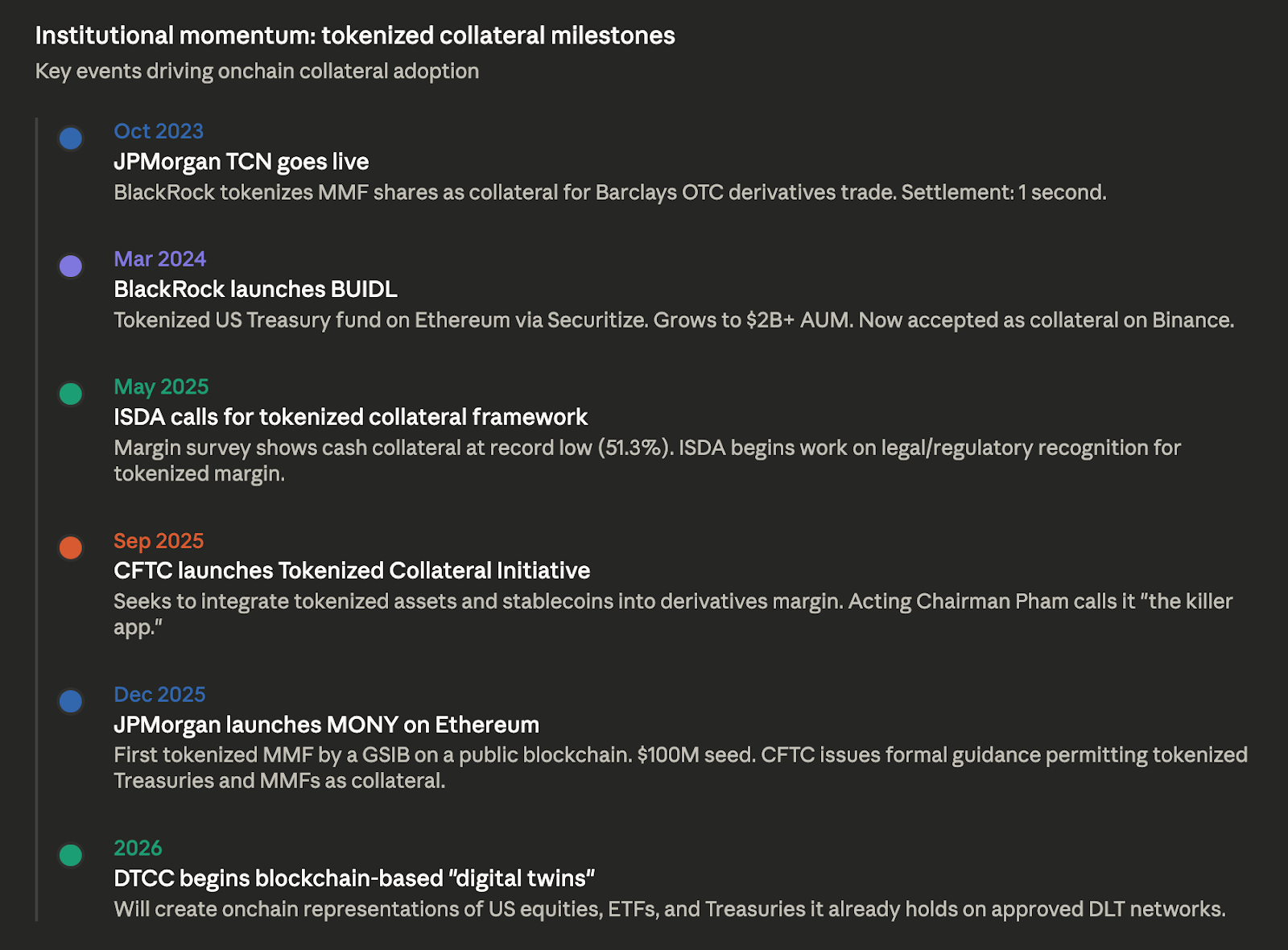

When JPMorgan's Tokenized Collateral Network settled its first live trade in October 2023, with BlackRock tokenizing money market fund shares as collateral for a Barclays OTC derivatives trade, the transfer took only one second. The same operation through legacy rails takes up to two business days.

By 2025, the largest banks in the world had moved to production.

JPMorgan launched its MONY tokenized money market fund on Ethereum in December 2025, seeded with $100 million of its own capital, the first such vehicle by a Global Systemically Important Bank on a public blockchain. Its Kinexys digital assets network has now processed over $1.5 trillion in tokenized transactions, averaging $2 billion daily. BlackRock's BUIDL fund, a tokenized US Treasury product, has grown past $2 billion in AUM and is now accepted as off-exchange collateral on Binance. Franklin Templeton's BENJI fund pioneered the category. Goldman Sachs and BNY Mellon have partnered on tokenized money market fund shares for institutional investors. Tokenized fund AUM more than doubled in 2025, growing from $4 billion to over $8.6 billion by year-end.

But this convergence isn't one-directional. While banks are tokenizing traditional assets to move them onchain, onchain-native protocols are building the collateral infrastructure to receive them.

Falcon Finance has built sUSDf as the yield-bearing layer on top of USDf, a synthetic dollar minted against a diversified basket of collateral ranging from stablecoins to tokenized collateral. As of March 2026, USDf supply stands at $1.63 billion, backed by $1.78 billion in reserves. This comes as regulators and market bodies begin defining frameworks for tokenized collateral, from stablecoins to U.S. Treasuries and money market fund shares.

In September 2025, the CFTC launched its Tokenized Collateral and Stablecoins Initiative, explicitly targeting the integration of tokenized assets into derivatives margin frameworks. Acting Chairman Caroline Pham called collateral management "the killer app" for tokenized markets. By December 2025, the CFTC had issued formal guidance permitting tokenized US Treasuries and money market fund shares as collateral for futures and swaps, alongside a pilot program accepting Bitcoin, Ethereum, and USDC as margin.

ISDA is working with eight trade associations to establish legal and regulatory frameworks for tokenized collateral.

The DTCC will begin creating blockchain-based "digital twins" of securities it already holds starting in 2026, including US equities, ETFs, and Treasuries.

This is no longer experimental. The largest banks, the largest asset managers, and the primary regulators are building toward the same destination.

The scale of what is coming

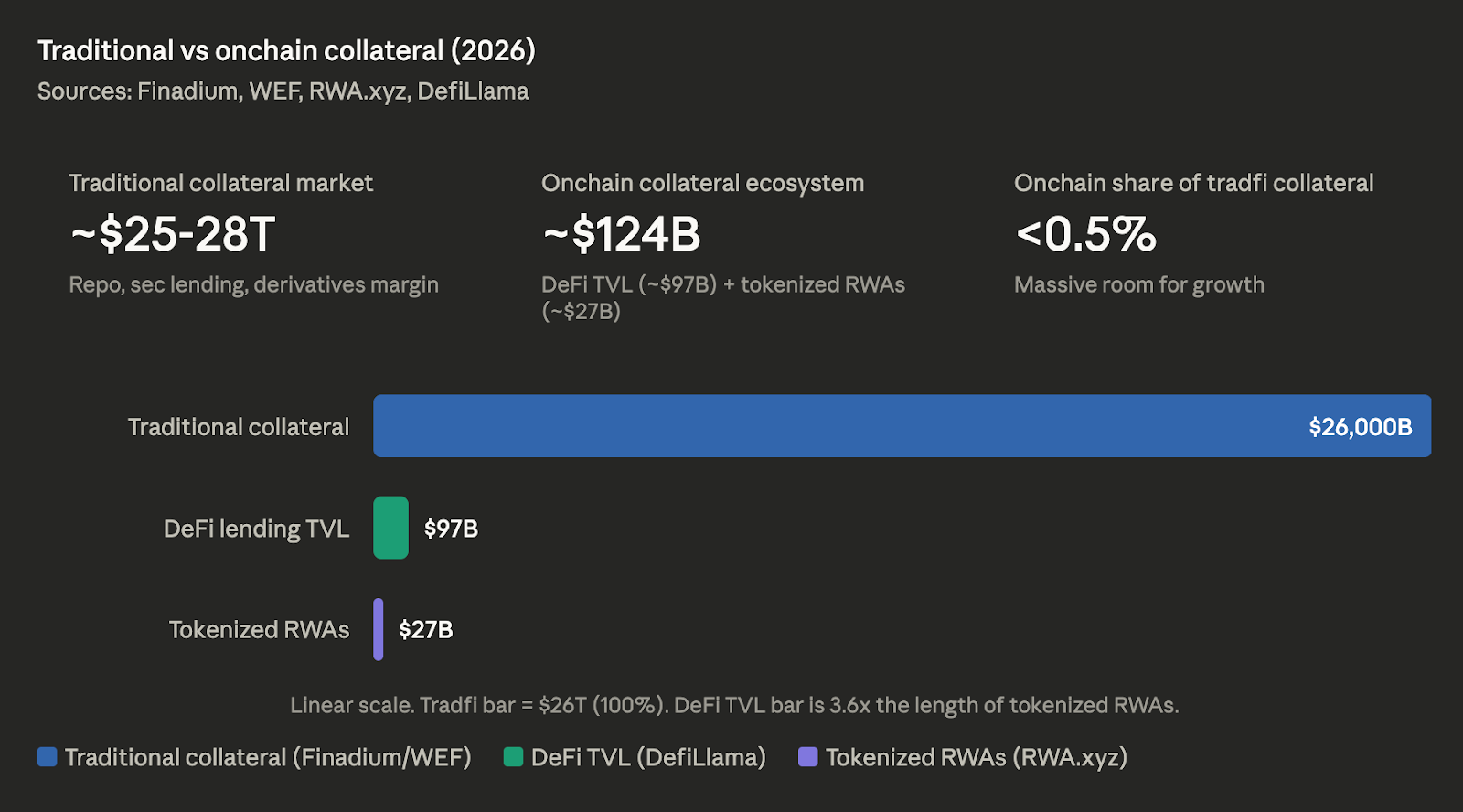

Onchain collateral today remains a fraction of traditional markets. It represents less than 0.5% of traditional collateral markets. Tokenized real-world assets (excluding stablecoins) sit at approximately $27 billion according to RWA.xyz, having grown over 2,200% since 2020. DeFi lending protocols hold roughly $97 billion in total value locked according to DefiLlama.

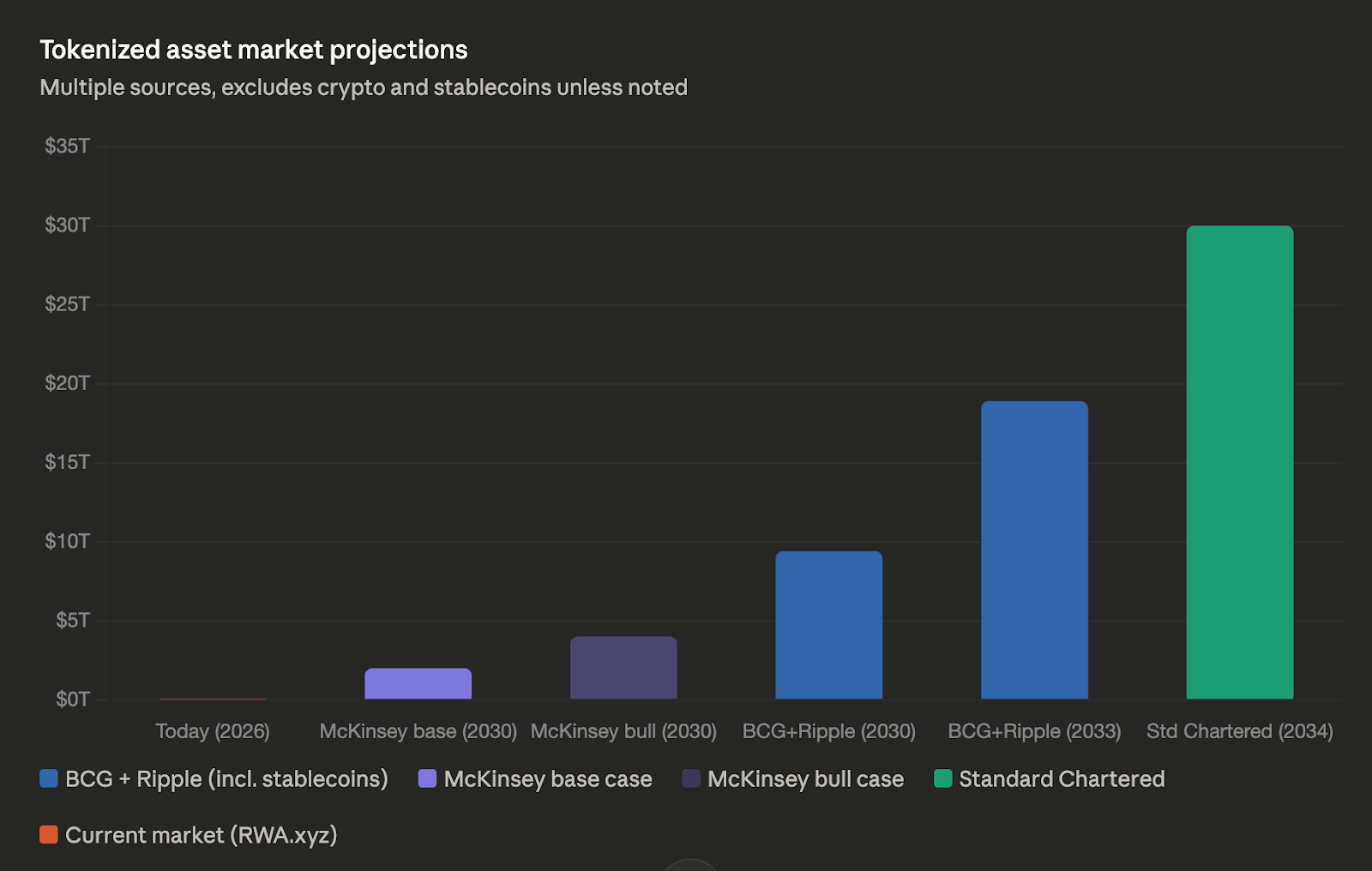

The projections for where this goes are directionally consistent even where they differ in magnitude.

McKinsey projects $2 trillion by 2030 in its base case. BCG and Ripple project $18.9 trillion by 2033, while Standard Chartered forecasts $30 trillion by 2034.

Even McKinsey's conservative floor of $2 trillion by 2030 would represent a 40x expansion from today. But the more significant number is the collateral eligible for this expansion. If tokenization converts even 5% of the $204.5 trillion eligibility gap into mobilizable collateral, that is $10 trillion in newly usable capital. The impact on margin efficiency, funding costs, and balance sheet optimization runs into the hundreds of billions annually.

Three structural shifts to prepare for

Settlement compression

Every institution holds excess liquidity to bridge the gap between margin calls and collateral settlement. That gap is closing. As collateral moves in seconds rather than days, much of that buffer capital becomes redundant. Across the derivatives market, this trapped capital runs into the hundreds of billions.

Collateral expansion

Tokenized Treasuries, money market fund shares, private credit, tokenized equities, and yield-bearing synthetic dollars become programmable collateral and rehypothecatable through smart contracts with embedded compliance.

Cross-border convergence

Moving collateral across jurisdictions currently requires correspondent banks, multiple custodians, and multi-day settlement. The Canton Network's 2025 research found 1 to 3% pricing gaps for identical assets across chains and 2 to 5% friction costs for cross-chain capital movement. These are engineering problems with known solutions, not structural limitations.

The window for positioning is now

The strategic question is the same wherever you sit: are you building the infrastructure, partnerships, and operational readiness to participate in this collateral layer, or adapting to standards set by those who moved first?

For onchain-native institutions, it comes down to whether your protocol can serve as the collateral layer TradFi needs while remaining composable and capital-efficient enough for institutional-scale flows.

The $204.5 trillion eligibility gap will not survive the decade. The only question is how much of it the early movers capture.