The Onchain RWA Landscape in 2026

Published • 29 Apr 2026

8 mins

.png%3Fprefix%3Dmedia&w=3840&q=75)

How the Collateral Layer Is Coming Into View

A year ago, the question in RWAs was whether traditional finance could actually put real assets on-chain. They did. Distributed tokenized value now sits at $30.5B as of April 29, 2026, roughly 4x where it was twelve months ago. Five tokenized Treasury products sit above $1B. BlackRock, Franklin Templeton, Janus Henderson, Apollo, and Ondo are running live products, not pilots.

Issuance was the hard problem, and it got solved faster than most people expected. The interesting question now is whether these assets will actually get used once they're on-chain. The answer is starting to look like yes, and the mechanism is collateral.

Tokenized Treasuries are moving from static yield products into active components of lending, repo, and margin systems. JPMorgan's Onyx has reportedly processed close to $900B in digital assets through tokenized repo since launch. Credit platforms are stacking close to $3B in distributed value built around institutional lending structures. Stablecoins increasingly collateralize against tokenized Treasuries and flow through the same treasury operations. What looks like a collection of separate categories is actually starting to behave like a single capital layer, and that is where the next phase of growth comes from.

Treasuries Reached Scale, and Started Behaving Like Collateral

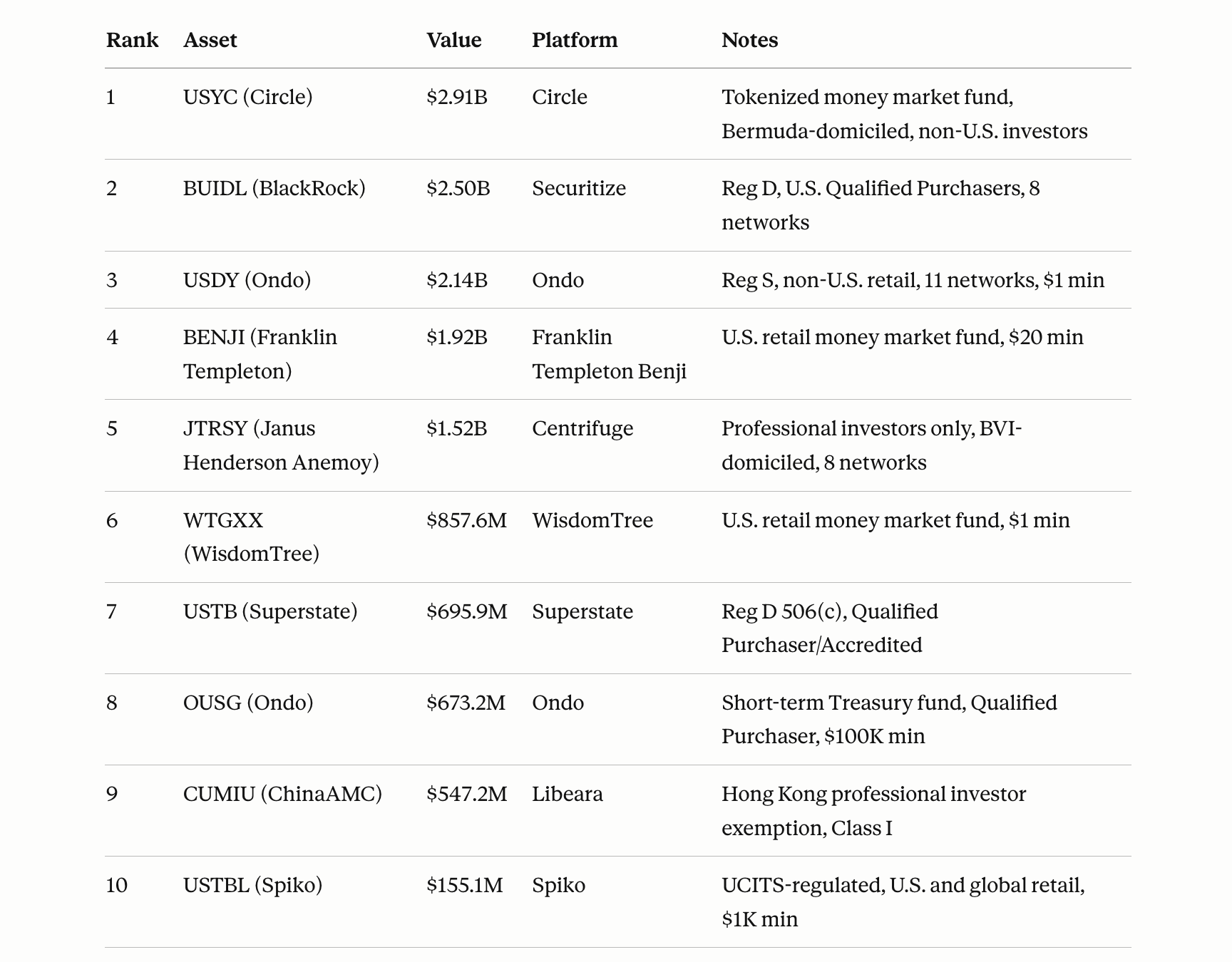

Tokenized U.S. Treasuries have been the anchor of the RWA market and remain so at roughly 45% of distributed value. The top 10 Treasury products exceed $10.9B, and five products now sit above $1B. A year ago, only BlackRock's BUIDL was near that threshold.

The shift that matters is what is happening to these products once they are issued. Circle's USYC has climbed nearly 40% in 30 days to $2.6B, overtaking BUIDL as the top tokenized Treasury. A meaningful share of that growth has come through BNB Chain, which is up 31% in the past 30 days to $3.4B and now the #2 RWA network, driven partly by USYC deployment. Janus Henderson's JTRSY on Centrifuge grew 83.65% in the same period and crossed $1B, which validates Centrifuge's pivot toward institutional fund infrastructure. BUIDL remains at $2.1B across eight chains with over $100M in cumulative yield distributed. Ethereum still sits at 58% of total RWA network share, though its share is declining as Treasuries move multi-chain.

APYs cluster between 3.17% and 3.82%, tracking underlying T-bill yields. That return profile is not dramatic on its own, which is the point. The value of these products is shifting from the yield itself to how easily they can be used as collateral. JPMorgan's Onyx processing $900B in tokenized repo is the institutional version of the same pattern. The yield is table stakes. The reusability is what makes these products interesting.

Stablecoins Are Already Part of the Same System

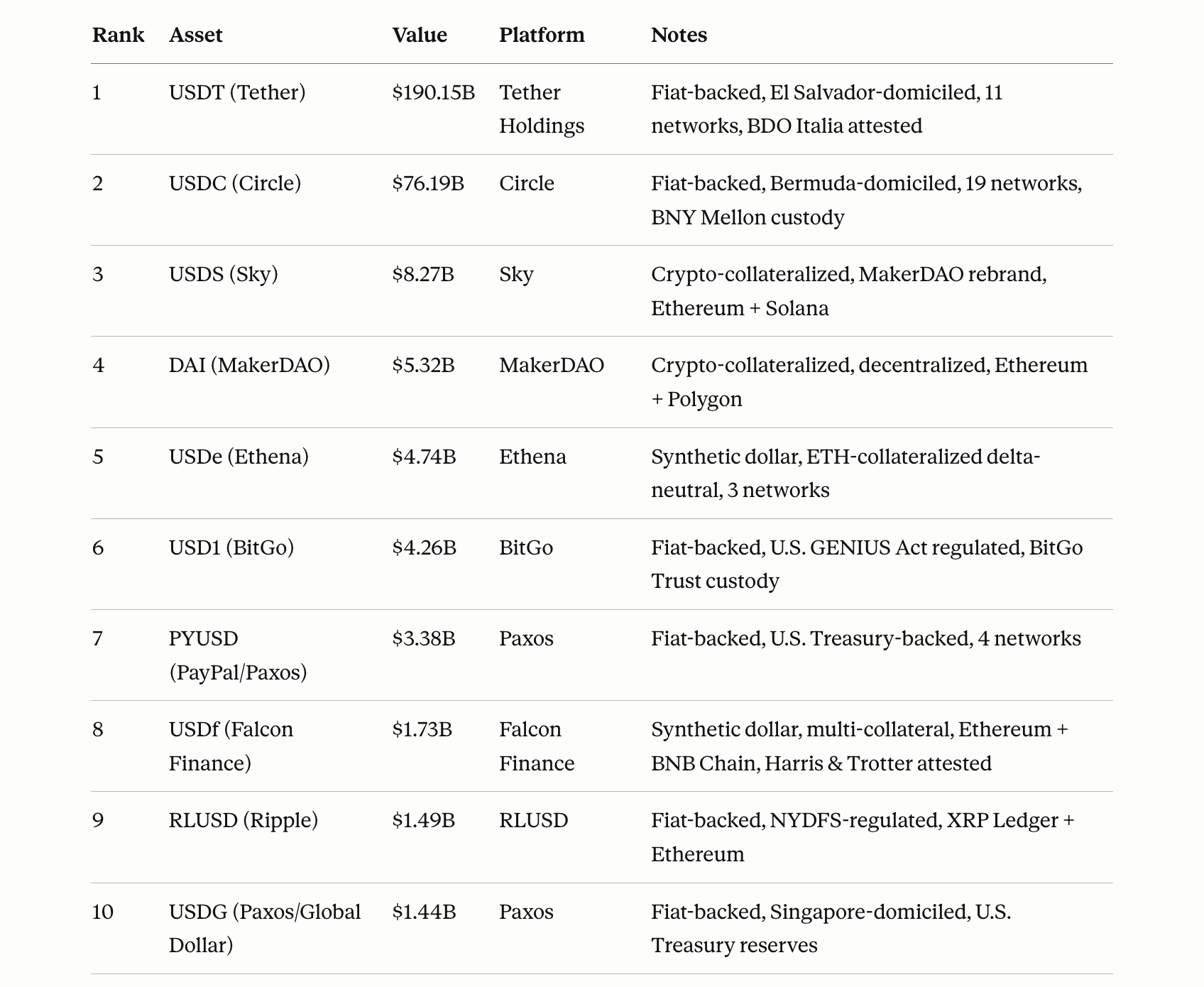

Stablecoin supply is around $305B, with USDT and USDC continuing to dominate. What makes the stablecoin story relevant to the collateral thesis is that stablecoins and tokenized Treasuries increasingly function as parts of the same system rather than parallel categories.

USDf sits at #8 globally at $1.7B, ahead of Ripple's RLUSD and Paxos' USDG. The protocol is less than 12 months old and backs USDf partly against tokenized Treasuries, which is a clean example of the collateral layer in action. USYC flows through stablecoin treasury operations. Falcon has added tokenized Mexican T-bills (CETES) as collateral for minting USDf, which extends access to non-U.S. sovereign yield through the same mechanism. USDe (Ethena) remains the leader in yield-bearing synthetic dollars at $5.9B. USD1 (World Liberty Financial) has surged to $4.4B.

The categories blur at the edges precisely because the infrastructure is converging. A stablecoin backed by tokenized Treasuries, used as payment collateral in DeFi, is not really a different product from a tokenized Treasury used as margin. It is the same asset wearing a different wrapper, and that is what makes the system work.

Credit Is Where the Growth Goes Next

Treasuries made RWAs legible to institutional investors. Credit is where the growth is because it is where the differentiation lives.

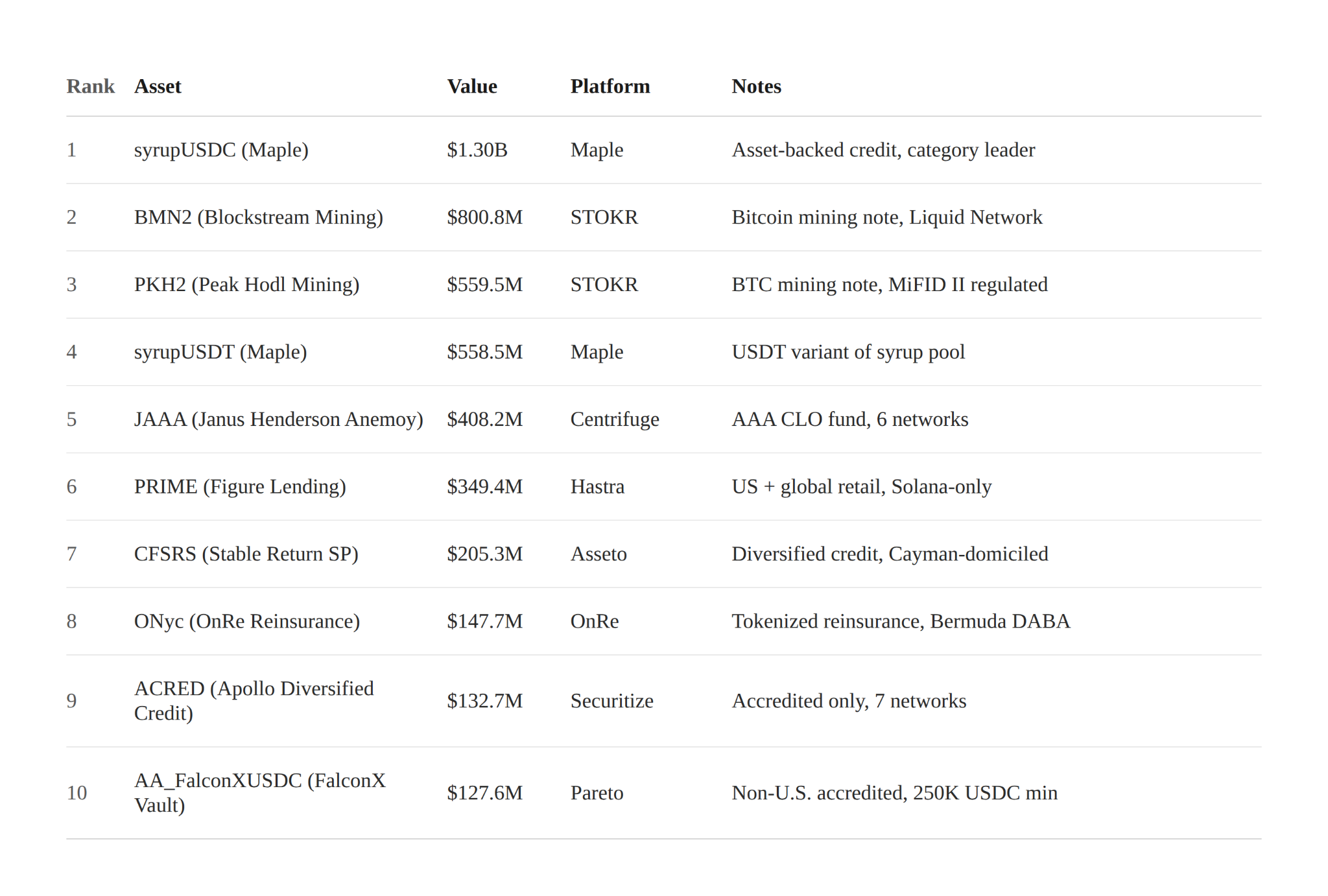

Onchain private credit stands at roughly $5.2B in distributed value, with broader counts that include represented and platform-locked assets closer to $18-19B. Treasury yields are uniform. Credit yields depend on structure, underwriting, and counterparty quality, which creates space for platforms to build competitive products.

Maple Finance has emerged as the dominant distributed credit platform, with syrupUSDC ($1.30B) and syrupUSDT ($558.5M) together representing over $1.85B in combined value. STOKR sits in second place on the back of Bitcoin mining. Blockstream's BMN2 ($800.8M) and Peak Hodl's PKH2 ($559.5M) together add up to roughly $1.36B, making BTC mining-backed credit quietly the second-largest category. Centrifuge anchors the institutional tokenized credit infrastructure with Janus Henderson's JAAA AAA CLO fund at $408M across six blockchain networks. The reason credit matters for the broader thesis is that these products are already being used within DeFi lending systems, stablecoin collateral structures, and institutional yield strategies. They plug into the same collateral layer Treasuries are helping to build, and they offer yield that Treasuries cannot match. If the thesis is correct, credit is where the next wave of distributed value gets booked.

The reason credit matters for the broader thesis is that these products are already being used within DeFi lending systems, stablecoin collateral structures, and institutional yield strategies. They plug into the same collateral layer Treasuries are helping to build, and they offer yield that Treasuries cannot match. If the thesis is correct, credit is where the next wave of distributed value gets booked.

Equities Are the Next Category to Plug In

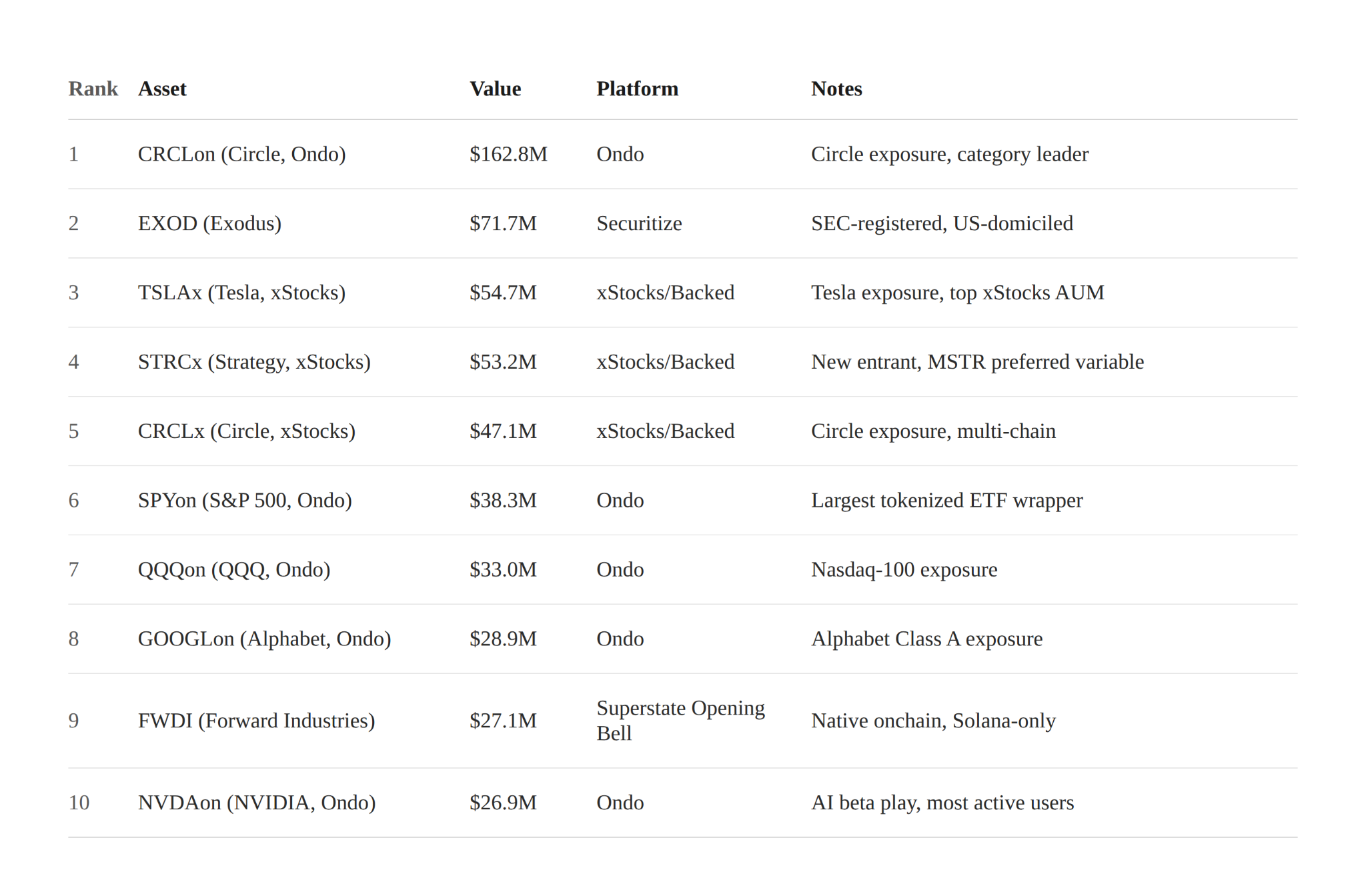

Tokenized equities are still early at around $1.1B in total category value, but the trajectory is steep. RWA.xyz tracks over 2,099 tokenized stocks as of mid-April 2026. Ondo and xStocks have emerged as the two dominant platforms.

Ondo holds multiple products in the top 10, including CRCLon (tokenized Circle stock, category leader), SPYon, MUon, NVDAon, and QQQon. Ondo Global Markets launched in early 2026 with over 100 tokenized US stocks and ETFs and plans to scale to thousands. xStocks, now part of Kraken following its acquisition of Backed Finance, is the second major platform. The reason equities matter within the thesis is not the current size. It is what unlocks when they can be used as collateral. Today most tokenized equities are exposure products, useful for 24/7 access and fractional ownership but not yet integrated into lending or margin systems. The moment regulation allows tokenized equities to sit alongside Treasuries in the collateral layer, they become meaningfully more connected to the rest of the system. That is the scenario the GENIUS Act, CLARITY Act, EU MiCA, Singapore VCC, and UAE VARA frameworks are collectively moving toward.

The reason equities matter within the thesis is not the current size. It is what unlocks when they can be used as collateral. Today most tokenized equities are exposure products, useful for 24/7 access and fractional ownership but not yet integrated into lending or margin systems. The moment regulation allows tokenized equities to sit alongside Treasuries in the collateral layer, they become meaningfully more connected to the rest of the system. That is the scenario the GENIUS Act, CLARITY Act, EU MiCA, Singapore VCC, and UAE VARA frameworks are collectively moving toward.

A newer adjacent category, Active Strategies, has also emerged on RWA.xyz, capturing onchain fund strategies beyond passive yield or static credit. USCC (Superstate Crypto Carry Fund, $201M) runs an active basis trade onchain at 5.67% APY. MI4 (Mantle Index Four, $129M via Securitize) is an index product. The size is small, but the category shows institutional-grade active management starting to migrate on-chain rather than staying in traditional fund wrappers.

Where the Thesis Does Not Hold Yet

Not every RWA category has converged on collateral utility. The categories that have lagged are worth flagging because they tell you what the next unlock looks like.

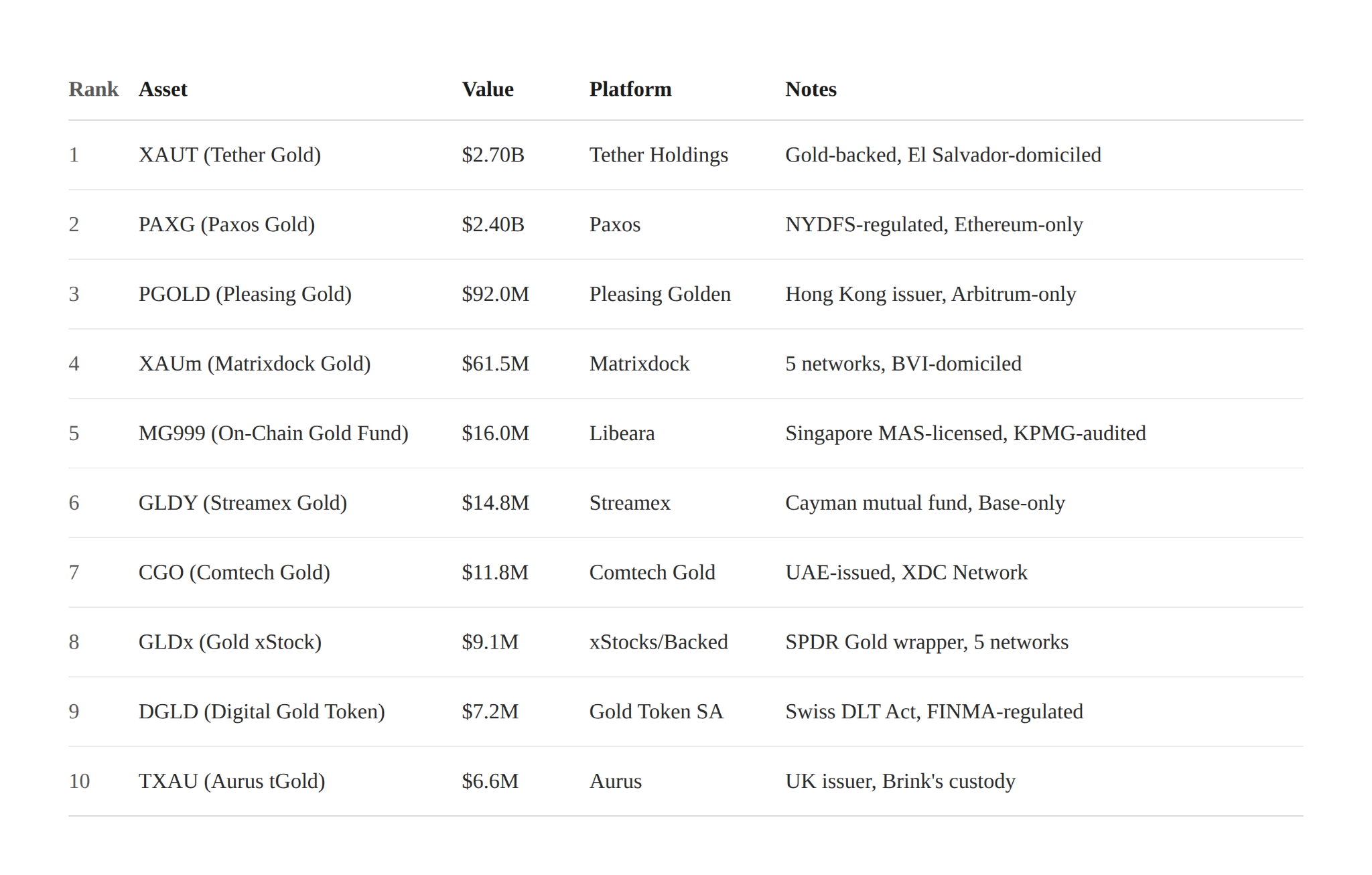

Distributed commodities sit at $5.42B, up 8% over the last 30 days and roughly 3x from early 2025 levels. Gold dominates: Tether Gold (XAUt) and Pax Gold (PAXG) together account for $5.10B, or over 95% of the distributed category. Outside this, represented commodity assets add another $1.96B, including Justoken's ~$1.7B in green financing and agricultural tokens, and Ctrl Alt's $281M in tokenized diamonds. The category is growing, but most products are structured as exposure rather than as collateral assets, which caps how much utility they can drive within the broader system.

In other categories, non-U.S. government debt sits at roughly $1.3B, with Spiko's EUTBL dominating at $916M. The CETES example inside USDf is the clearest case of non-US sovereign debt being pulled into the collateral layer, but the broader category remains small.

Private equity and venture capital remain under $1B in distributed value. Securitize dominates with BCAP ($209M, the largest tokenized VC fund) and EXODB ($124M). Most products are illiquid with limited secondary trading, which is the opposite of what the collateral thesis requires.

Real estate is the most underpenetrated category relative to its total addressable market, at around $300M with no single product crossing $100M. The complexity of property management, legal structuring, and variable liquidity keeps it well behind. Tokenized real estate is probably not a meaningful category before 2030.

The pattern across all of these is the same. Categories where the assets can move and be reused are scaling. Categories where they cannot are stuck.

What the Collateral Layer Unlocks Next

The argument running through this piece is that RWAs are moving from something investors hold to something that is used. That transition is where the next phase of growth comes from.

Treasuries started as a yield product and are now being used across lending, repo, and margin systems. JPMorgan's Onyx and DeFi protocols are pulling at the same thread from different ends. Credit is where the yield and differentiation live, and where the distributed value is accumulating fastest right now. Stablecoins are already operating inside the same collateral framework. Equities are the next category to plug in, pending the regulatory frameworks currently in progress.

Step back and the pattern is straightforward. Yield was the entry point. Collateral is what unlocks the next phase. What comes from here depends on whether the infrastructure being built now makes these assets work harder than their offchain equivalents, or just mirrors them in digital form. The data suggests the former is starting to happen.