April 2026: TSLAon joins as collateral, and we make the case for the $205T eligibility gap

Published • 30 Apr 2026

5 mins

.jpg%3Fprefix%3Dmedia&w=3840&q=75)

April was a month of widening the door. We added TSLAon as collateral, kept reserves transparent, and put out two of our deepest pieces yet on where the RWA market actually is and why most of the world's marketable securities still can't move as collateral. If you've been with us for a while, you'll recognize the throughline: synthetic dollars only matter if the rails underneath them are real. We spent April making those rails wider.

USDf & sUSDf Updates

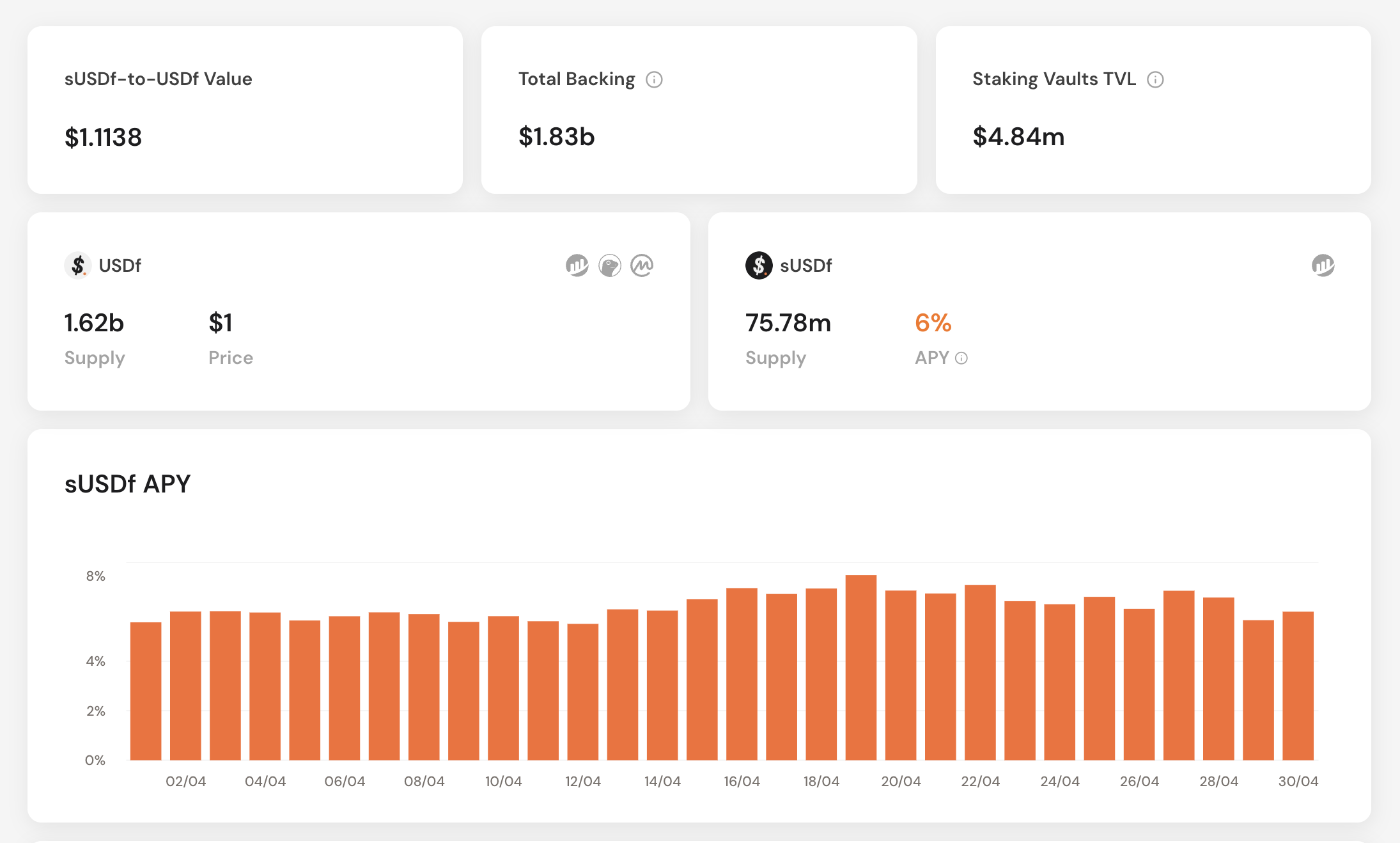

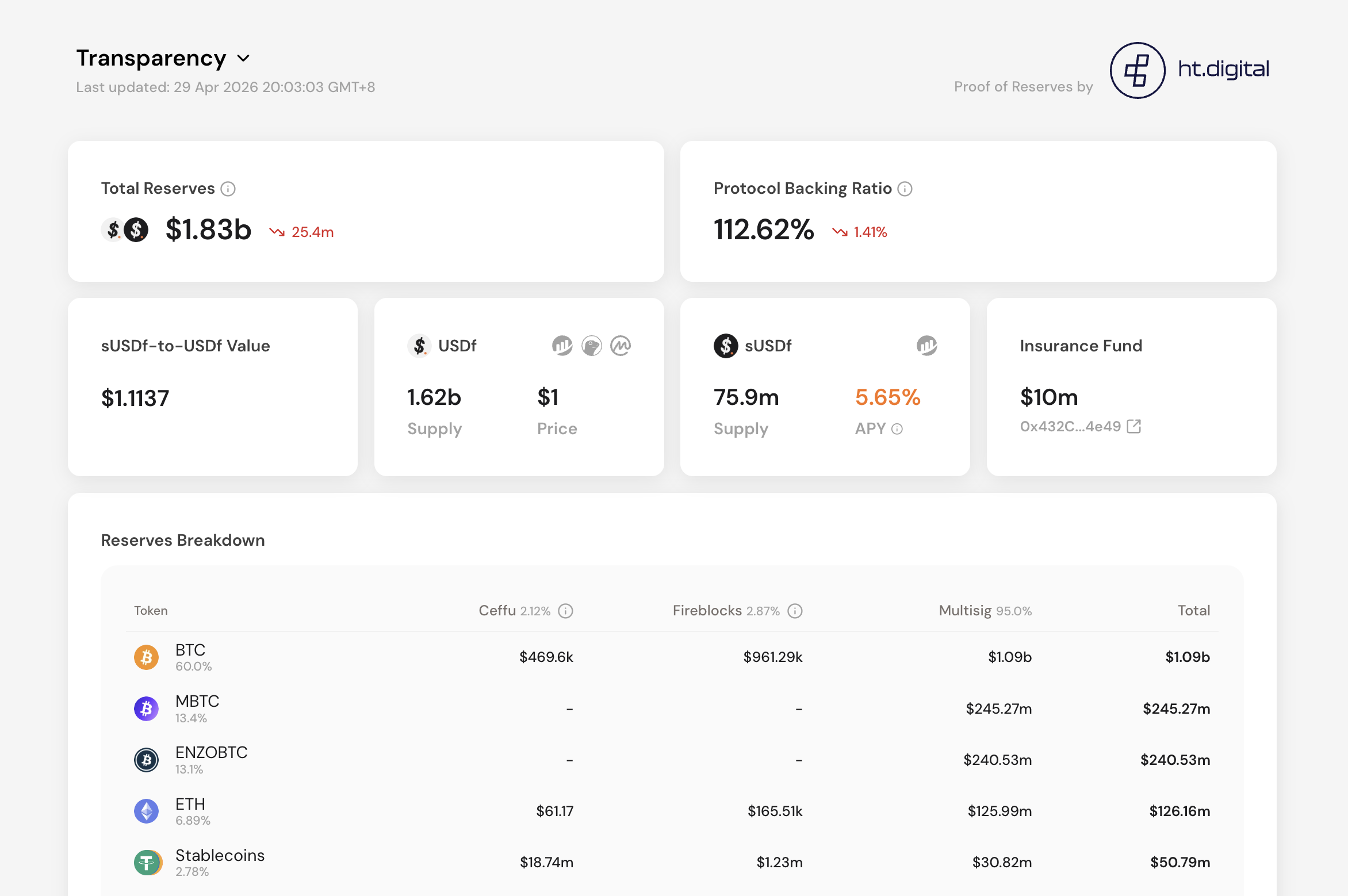

As of April 30, USDf supply sits at $1.62 billion, with $75.8 million in sUSDf. Total reserves are $1.83 billion, putting our backing ratio at 110.82%, confirmed by HT Digital's latest attestation on April 27. sUSDf is delivering 6% APY.

A few more things you'd probably want to know:

- Where the reserves sit: BTC at 59.9% ($1.09B), MBTC at 13.4% ($245.3M), ENZOBTC at 13.1% ($240.5M), ETH at 6.84% ($126.2M), stablecoins at 2.78% ($50.79M), and a smaller allocation across select altcoins.

- How yield is generated: options-based strategies make up 61%, positive funding farming and staking another 21%, with the rest spread across statistical arbitrage, spot/perps, cross-exchange arb, negative funding, and extreme movements trading.

- On custody: 95% sits in multisig, with the remaining 5% split between Ceffu and Fireblocks.

Key Announcements

TSLAon now live as USDf collateral

On April 23, we integrated TSLAon, our first Ondo tokenized asset. You can now mint USDf against TSLAon holdings using customizable risk parameters, which means you keep your upside exposure to the underlying while unlocking onchain liquidity. From there, USDf can be staked into sUSDf for variable yield, or deployed across the wider ecosystem. Get started here.

Tokenized equities are more useful as collateral than as 24/7 exposure, and that's the part we're building toward.

Ecosystem Growth and Partnerships

Working with Ondo

The TSLAon integration is our first incorporation of an Ondo tokenized equity, and it widens what counts as productive collateral on Falcon. We're treating it as the start of a longer conversation, not a one-off.

Where the RWA market actually is

The RWA market kept building momentum through April. A few numbers worth carrying around:

- $2.3 billion in open interest on Hyperliquid RWA trades.

- Distributed RWA value approaching $30 billion across 20+ chains.

- Ethereum still anchors the category at roughly 55%, with the top five chains accounting for 85% of the total.

Insights, Media and AMAs

The onchain RWA landscape in 2026

We closed out the month with our deepest market piece yet, mapping where the onchain RWA market actually sits in 2026. The headline number is $30.5B in distributed tokenized value as of April 29, roughly 4x where it was a year ago. Five tokenized Treasury products now sit above $1B, and BlackRock, Franklin Templeton, Janus Henderson, and Ondo are all running live products that continue to grow.

The piece walks through how Treasuries are moving from static yield products into active collateral inside lending, repo, and margin systems, why credit is where the next wave of growth shows up, where stablecoins fit into the same collateral framework (with USDf at #8 globally), and what unlocks when tokenized equities can finally sit alongside Treasuries as collateral. It also addresses the categories that aren't there yet and why. Read the full landscape.

$230 trillion in assets. Only 11% eligible as collateral.

Earlier in the month, we published a companion piece on the $205 trillion gap between global marketable securities and assets that can actually be used as collateral today. The article walks through what JPMorgan is doing with one-second tokenized collateral settlement and the MONY launch, BlackRock's BUIDL crossing $2 billion in AUM, the CFTC's moves on tokenized Treasuries and money market funds as margin, and ISDA's legal frameworks. We then map where USDf and sUSDf fit in that picture. Read the full article.

Stablecoins overtake ACH

We highlighted February 2026 data showing stablecoins clearing $7.2 trillion in monthly volume, edging past the U.S. ACH system's $6.8 trillion for the first time. The stablecoin market cap also touched a fresh all-time high near $320 billion.

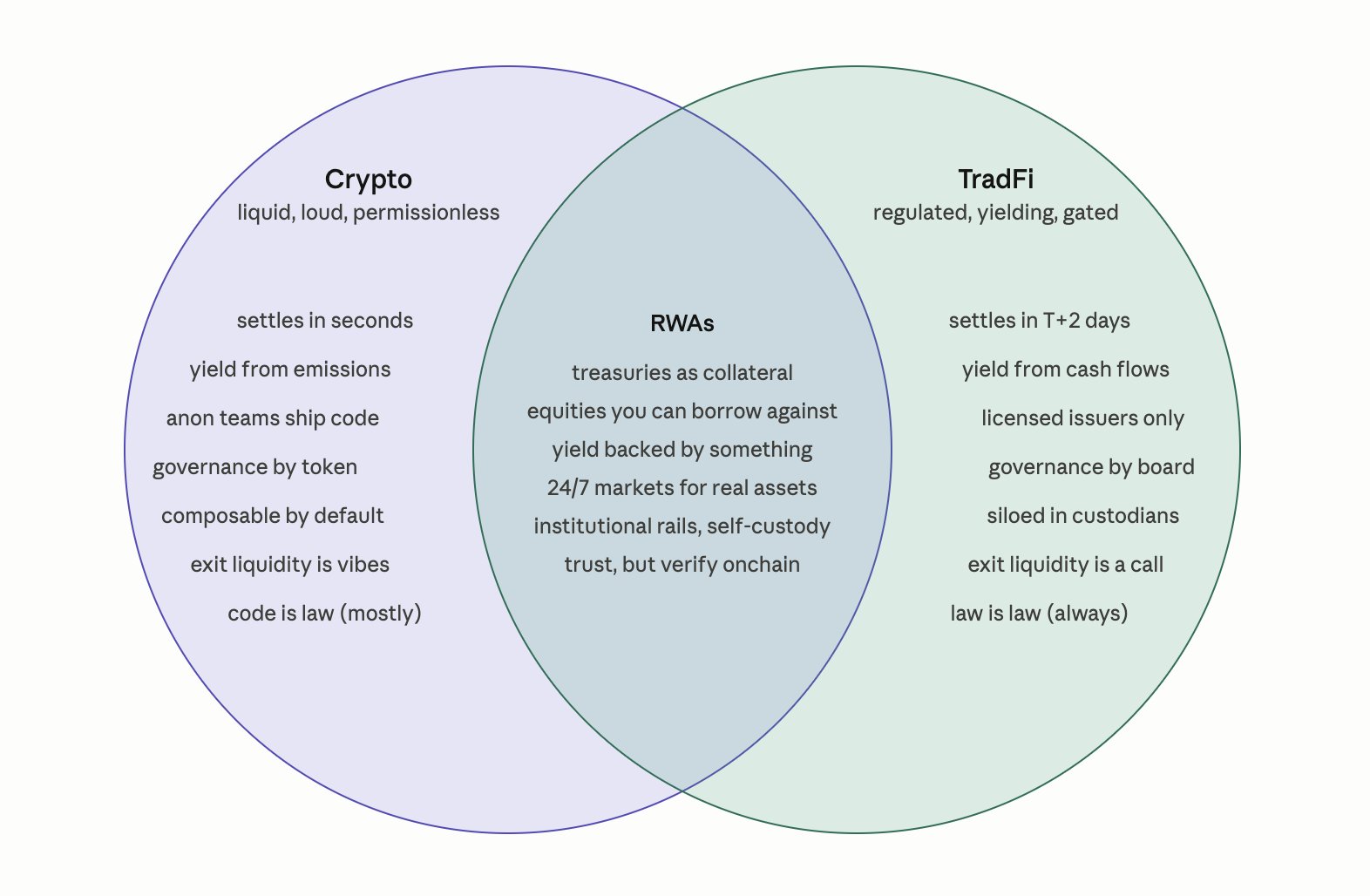

The RWA thesis, in one diagram

We shared a Venn diagram capturing where we think the action is: the intersection of yield, compliance, liquidity, and real economic utility. That's the corner of the chart trillions of dollars are starting to move toward, and where compliant collateral systems become non-optional infrastructure.

Tokenization as a structural shift

We picked up the IMF's recent paper framing tokenization as a "structural shift in financial architecture" and used it to make a related point we keep coming back to: dollar yield is scarce, dollar access isn't. Synthetic dollars exist to close that gap, and USDf is our take on how.

What's Next?

Looking ahead to May, we're widening the collateral set, going deeper on the RWA integrations already in motion, and we may have a partnership announcement to share before month-end. Reserves stay visible, as always. Thanks for being here for it!